![]()

20 Oct, 2021

As per Section 3 of the Indian Trust Act 1882, “a Trust is defined as an obligation annexed to the ownership of property and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him, for the benefit of another and the owner.” Simply put, Trust is nothing but the transfer of property by the owner (Settler) to another person (Trustee) on whom the owner has confidence for the benefit of a third person (Beneficiary). The Settler should legally transfer ownership of the property to the Trustee. In this blog, we shall discuss in detail about checklist for Trust registration and the process of Trust registration in India.

Trust serves as a way of contributing to the needs of the underprivileged. Generally, there’s a notion that Trusts are only to be created by the elite sector of society. However, this is not the case; a Trust can be created by ordinary men and women. Further, Trusts are classified into two categories namely Public Trust and Private Trust The provisions of the Indian Trust Act, 1882, governs only private trusts. On the other hand, Public Trusts are usually governed by state-specific legislation. It is to be noted that the Indian Trust Act is not applicable in Jammu and Kashmir and Andaman and Nicobar Islands.

Settler: A Settler is a person who creates the Trust by placing a certain asset that he/she owns into the Trust. Settler is also known as Trustor or Grantor.

Trustee: A Trustee holds the assets for the benefit of the Beneficiary. While in complete charge of the trust assets, the Trustee is under a legal obligation to maintain the trust property in the best possible way for the benefit of the beneficiaries. The Trustee is legally prevented from using the trust asset for his own ends.

Beneficiary: The Beneficiary is the third party who enjoys the benefit of the Trust property held and managed by the Trustee. The Beneficiary or beneficiaries may be either named in the Trust Deed or maybe a sufficiently defined group of persons (for example, “all children and grandchildren”).

READ Income Tax Exemption for Trust under Income Tax ActTrusts are further classified into two types, namely Private Trust and Public Trust. The Indian Trusts Act, 1882 [1] , manages private Trusts, whereas, on the other hand, Public Trusts are further divided into charitable and religious trusts. Public Trusts are usually governed by state-specific legislation, such as the Bombay Public Trust Act, 1950, etc. Moreover, Trusts can also be used as a vehicle for investments, such as mutual funds and venture capital funds. Such Trusts are governed by the Securities and Exchange Board of India (SEBI).

Following is the classification of Trusts in terms of the motive of formation:

Public Trust: A Public Trust is created for the benefit of the general public or a particular class of people. Thus, beneficiaries in the case of Public Trust are the general public at large. Public Trust is further classified into two parts i.e., Public Charitable Trust and Public Religious Trust.

Private Trust: A Private Trust is created by the Settler for the benefit of one or more particular individuals as its Beneficiary. Hence, a private trust is the one whose beneficiaries include families or individuals. For example, a trust created for relatives and friends of the Settler.

A Trust can be created by:

Following is the list of documents required for Trust registration:

Proof of the registered office address, such as an electricity or water bill.

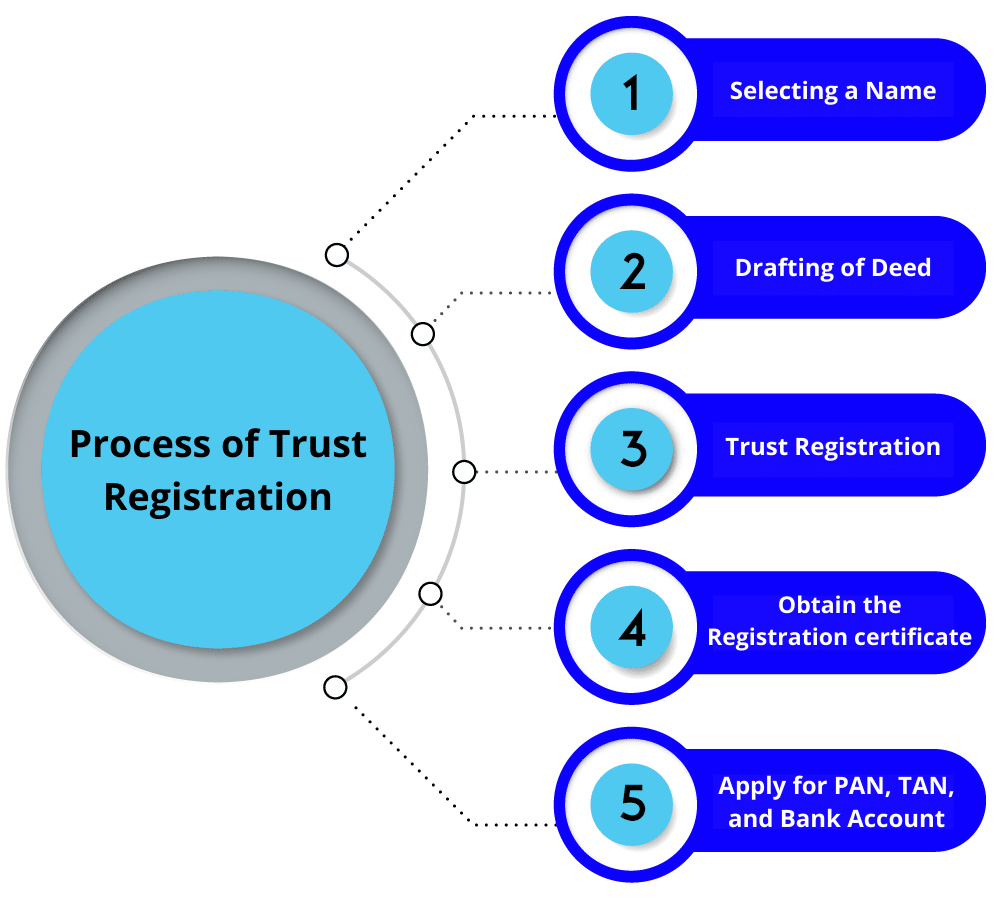

Following steps are to be followed to complete the process of Trust Registration:

The first step towards Trust Registration is selecting a unique name for your Trust. The name selected should not violate or infringe someone else’s name or trademark.

There should be atleast 2 trustees to create a Trust. However, there is no such bar on the maximum numbers of trustees required for a trust. The Settler cannot be the trustee and should be residing in India.

The next step is to draft a ‘Trust Deed’. The ‘Trust Deed’ has to be executed on appropriate non-judicial stamp paper, where the rate of stamp duty differs from state to state. The Settler is required to put his signature on every page of the photocopy of the Trust Deed. Moreover, it is compulsory for the settlers as well as the two other witnesses to be physically present along with their identity proof at the time of registration. Memorandum of Association should be drafted as it provides for the relationship between the trustor and trustee.

The next step is to obtain an appointment with the sub-registrar office having jurisdiction based on the registered office of the Trust.

Once you have drafted the ‘Trust Deed’ the next step is to present the deed before the registrar of the trusts having jurisdiction. After presenting the deed before the registrar, the further Trust Registration process is undertaken by the office of the sub-registrar.

Once you have submitted the Trust Deed with the registrar, the registrar keeps the photocopy and returns the original registered copy of the Trust Deed.

After completing all the formalities involved in the trust Registration process, the registration certificate is issued within a minimum of seven working days.

The final step in Trust Registration is to apply for the allotment of PAN number and TAN. Further, apply for the Bank Account in which all donations shall be deposited.

Section 12-A of Income Tax Act

The Income-tax Department issues 12A certificate to Trusts or NGOs. Any organization that has a 12A Certificate is not liable to pay Income Tax for an entire lifetime on its surplus income.

What is Section 80-G of the Income Tax Act?

If an organization has obtained an 80-G Certificate, then donors of that NGO can claim exemption from Income Tax.

The application for registration under section 12A and 80G can be applied just after the registration of NGO, and the application has to be applied to the Commissioner of Income-tax (Exemption) having jurisdiction over the institution.

All above mentioned checklist for trust registration should be complied with. If you wish to run an NGO, the most preferred way is to form a public charitable trust. Moreover, the process of Trust registration in India is simple and requires less documentation. The primary document needed for Trust Registration is ‘Trust Deed.’ Our experienced team of advocates at Enterslice shall draft the ‘Trust Deed’ for you and help you to complete the process of Trust Registration and take care of all checklist for trust registration. For further assistance, feel free to contact us.